News

Personal Finance: Savers Protect Your Deposits From Bankrupting Banks and Quantitative Inflation

The Euro-zone continues to teeter over the edge of the financial abyss as bankrupting countries that cannot print Euro's threaten the collapse of its banking system that would would soon collapse the whole global banking system in a matter of hours as electronic bank runs sweep across the worlds financial system resulting in trillions of dollars worth of deposits being withdrawn in a matter of hours and thereby collapsing first the Euro-zone and then within 24 hours the UK, USA and Asia along with it. My recent article (Euro-Zone Prepares to Print Trillions in Advance of Greece Debt Default) covered the potential consequences for the world in the event of financial armageddon, this article continues on from the last article that covered the inflationary depression consequences of money printing that the likes of Britain and the United States are engaged in and that the Euro-zone WILL eventually replicate (Bank of England's Quantitative Inflation Bankster's Paradise Inflationary Depression Economy ).

The focus of this article will be on concrete steps that depositors need to take now to reduce the real risk of the actual loss of their funds on deposits at bankrupting banks before they should go on to protect against the ongoing real terms loss of value in the face of the perpetual money printing Quantitative Inflation Mega-trend.

Banks Going Bankrupt - Lehman's Bankruptcy Example

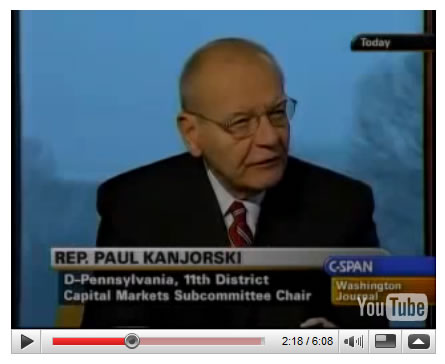

The 2008 Lehman's bankruptcy irrevocably changed the financial world as within a matter of days a chain reaction of the worlds banks and insurers were on the verge of going bust, pushing the world towards financial armageddon as the following video illustrates of just how close the U.S. Financial System came towards total collapse. At 2 minutes, 20 seconds into this C-Span video clip, Rep. Paul Kanjorski of Pennsylvania in February 2009 explains how the Federal Reserve told Congress members about a "tremendous draw-down of money market accounts in the United States, to the tune of $550 billion dollars." According to Kanjorski, this electronic transfer occurred over the period of an hour and threatened a further $5 trillion to be drawn out triggering a total collapse of the Financial System, which prompted Hank Paulson's emergency $700 billion TARP bailout action.

Video Served by Youtube

This is the real problem that the credit rating agencies, mainstream press and politicians are not stating which is that the fallout from sovereign default will not be orderly, yes the actual default process may be orderly, over seen and managed by the ECB with planned haircuts of first 20%, then 40% and then 60%, but the markets response won't be orderly, depositors will panic and pull their funds from those they perceive as having the greatest exposure to a. sovereign debt and b. to sovereign debt derivatives. THIS IS ALREADY HAPPENING. Which is the real reason why the banks are not lending, because they know they cannot unwind their over-leveraged positions in the event of default so have been hoarding cash now in advance of sovereign default.

Eurozone-zones Bogus Stress Tests Busted, Ignored Sovereign Default and the Derivatives Monster.

Today's financial system is in a worse state than when Lehman's went bust as measured by the credit default swaps, because there are multiple Lehman's out there ALL teetering on the brink of bankruptcy as a consequence of exposure to bankrupting PIIGS as the ongoing news coming out of Europe illustrates with the bailouts of Lehman wannabe's such as the French / Belgium bank Dexia and Greek banks. That's before we start to even approach the consequences of banks such as the German giant Deutsche Bank going bust.

All of the now failing banks passed the eurozone's bogus stress test that never took into account the obvious that Greece would eventually default on its debts and therefore the banks are sitting on losses of at least 50% on their Greek sovereign debt holdings, never mind losses on other PIIGS debt.

The reality is that virtually ALL of the European banks would fail the PIIGS defaulting and triggering haircuts of 40-60% of sovereign debt holdings which means the bank stress tests were pure political propaganda with no basis in reality.

The solution that the mainstream press obsesses over is for the recapitalisation of the banks, which theoretically should work though involve amounts far beyond anything being put forward today, i.e. you can forget Euro 100 billion, even Euro 250 billion, what would be needed are amounts north of Euro 500 billion. However as I have repeatedly warned over the years this does not address the real issue of ultimate exposure, which is not that of the PIIGS debt but that of the OTC derivatives market, which globally now exceeds $600 trillions as a consequence of over leveraged positions.

You can tell that the banks are sitting on huge losses (bad loans) when they are buying insurance against their own debt defaulting (credit default swaps) such as Goldman Sachs recent announcements of profits on this basis as a consequence of the increase in the value of the CDS on its debt.

The risks are that of how much is the ultimate liability once the PIIGS start to default and banks start to go bankrupt requiring recapitalisation bailouts, where will it end?

That question is unknown, it could stop at Euro 1 trillion, then again it may require Euro 10 trillion or Euro 100 trillion, I and no one else knows, and the risk is global because ALL banks swim in the same derivatives ocean where the sovereign debt exposures are mere tips of over leveraged ice-bergs. These are the un-quantifiable risks that the banking system is exposed to that depositors need to protect themselves against in the event of sovereign defaults.

Meanwhile, whilst the BBC more prone to regurgitating central bank propaganda as evidenced by the fact that the likes of BBC new broadcast of continuous statements as to why UK inflation is always destined to imminently start falling (for near 2 years now), recently let itself become infected by the dark side by letting a perma-bear trader wonder into the news studios :

"know the stock market is finished. The euro, as far as they're concerned, they don't really care".

"For most traders, we don't really care that much how they're going to fix the economy, how they're going to fix the whole situation our job is to make money from it," he said.

"Personally I've been dreaming of this moment for three years. I have a confession, which is I go to bed every night, I dream of another recession."

"The governments don't rule the world. Goldman Sachs rules the world. Goldman Sachs does not care about this rescue package, neither does the big funds."

It's interesting to see that the stock market is up over 10% since he spoke of a market crash!

Depositors Not Being Paid For Risk of Financial Armageddon

Even though a european banking crisis seems inevitable, I personally rate actual financial armageddon i.e. the banking system ceases to operate as a low probability as a consequence of unlimited money printing by the governments and central banks pumping an infinite amount of liquidity into the banking systems to avoid financial collapse at all cost (highly inflationary), however the problem with the Euro-zone is that it functions as a committee of 17 countries that literally takes months to respond to crisis, when they may only have hours to act!

For instance recently we witnessed the spanner in the works that the little Czech Republic had thrown as it initially rejected expansion of the European bailout fund because they did not want to contribute to a potential bailout themselves, despite the fact that for a decade the likes of the Czech republic had been gorging on vast quantities of E.U. financial aid, off course financial armageddon would hit the likes of small countries such as the Czech republic much harder as investors pulled out funds.

Against the current system of operation of the Euro-zone that appears designed for maximum effect for the potential for failure, depositors are just not being paid enough interest to to carry the risk of loss of capital, i.e. annual interest rates of between 1-3% (before tax) are just not enough for the real risks being carried for the nominal loss of the value of savings, therefore as I have iterated on several occasions during the past few years, and most recently in June (Bankrupt Greece Blackmails Europe, Bailout or Euro Zone Dies, Global Financial System Collapse) that depositors really do need to ACT BEFORE THE EVENT, because they will be unable to do so DURING THE EVENT.

UK Bank Downgrades, Now Rated Worse than Lehman's

The Moody's credit rating agency downgrade of 12 UK banks reminds readers that it's not just european mainland banks that are under pressure, but all banks across the globe, including the UK.

The downgrade is in response to the real risk that the UK government will no longer bailout all UK financial institutions in the event of default and bankruptcy.

Most notable downgrades were for the UK big banks:

- RBS from Aa3 to A2

- Lloyds TSB Aa3 to A1

- Santander Aa3 to A1

- Nationwide Aa3 A2

- Co-op A2 to A3

The downgraded banks in near unison stated that the downgrades do not make any difference to their businesses, well they would say that, instead as is the case with every borrower that if you become a higher risk then you pay a higher interest rate and more collateral is demanded against market derivatives positions, remember these banks are leveraged upto the hilt so small changes in ratings have huge impacts on their financial health. In fact a large part of the summer stock and commodities market correction can be put at the feet of banks having to liquidate assets to cover derivatives positions.

Also, remember that the credit agencies are BEHIND THE CURVE, the true state of the banks is far worse, for instance Lehman's was rated as A2 just days prior to its bankruptcy ! That's the same as RBS, Nationwide, and better than where Lloyds and Santander stand.

The trend towards bank bankruptcy continues since which time governments have edged closer towards bankruptcy themselves which has increased the risks of debt defaults.

Eurozone Meetings Trending towards a 2 trillion bailout. We have had eurozone meetings, after meetings after meetings for the duration of the sovereign debt crisis, where the underlying message coming through is that the banks need to be re-capitalised, with Germany wanting the banks to seek funds from private investors whilst France wants public funds involved, preferably central bank unlimited funding because of the exposure of French banks that risk bankrupting France itself and thus France ultimately requiring an IMF/ EU/ German bailout which was illustrated by the recent downgrade of French debt. There is no instant fix, the ratification of the Euro 440 billion pot is just sticking plaster, it is not enough, my expectations are for 2 trillion but the longer crises goes on then so will the ultimate costs and economic damage escalate.

The ratified 440 billion will have to be leveraged to at least Euro 2 trillion but that will still not be enough for when France comes knocking on the bailout door, still as I have earlier illustrated the banks if not stabilised now could result in a situation infinitely worse. Greece Default to Trigger PIIGS Wide Default When Greece defaults on its debts the rest of the PIIGS, Ireland, Portugal, Greece and Spain will all look at Greece being let off the hook, do the sums and come to the same conclusion that they should also follow the Greece example in an orderly default as opposed to being suckers that continue to pay for debt that they cannot afford.

Will Germany Pay the Bill ? Well Germany paid the bill for German unification which in real terms will ultimately be similar to the total cost of bailing out Europe, starting with Greece but probably ending with France itself.

Current State of the Banking Crisis

European Leaders have been meeting during the weekend where the objective is to agree to leverage the already agreed bailout fund higher to act as insurance for sovereign debt holdings to a certain percentage against default, therefore this increases liabilities without actually committing to put any money in the pot. However the risks are unknown, i.e. the risks could be Euro's 1 trillion, 2 trillion, or perhaps 3 trillion ? No one knows because the amount of sovereign debt outstanding continues to expand at the rate of about 500 billion euros per year across the Euro-zone and with it so does the banks derivatives exposure at between X10 and X30.

I won't admit to understanding exactly what the Euro-zone are agreeing to do because I don't think they want the people to understand the facts because the losses as a consequence of default will be many times the face value of the outstanding debt, so definitely serves the politicians not to mention the multi-trillion Euro liabilities being agreed to on behalf of the electorates, especially Germany, where politicians have already rejected calls for new monies, so smoke and mirrors are being used to achieve the same outcome, which at the end of the day bodes ill for the value of the Euro.

All I know is that the euro-zone ultimately are destined to follow the example of the UK and USA, that of monetizing debt in which respect the UK £275 billion Q.E. would translate into an ECB debt monetization of about Euro 1.5 trillion, so they do have the scope to make some major market moving announcements, if they are able to agree to do so.

PIIGS Debt Default Could Trigger Economic Booms The PIIGS are locked into the German backed Euro, which means currency downside is limited i.e. Greece are not going to experience the high inflation rates that the likes of Iceland experienced following its own default and currency crash. This gives the PIIGS a great opportunity that following the initial pain will result in a economic booms as debt interest burdens approaching total government revenues evaporate. Many academics out there put forward a multitude of reasons why default would be bad for the PIIGS i.e. such as they will no longer be able to borrow money on the world markets. Firstly, they don't need to borrow for the next few years because they have the likes of the German backed ECB to pump as much money as needed into the PIIGS to alleviate the initial pain of default. Secondly, the markets do not act on the basis of academic theories, the markets DISCOUNT the future and not dwell on the past, they will see the opportunities that will flow from future booms and soon FORGIVE the PIIGS defaults, this is after all the lesson of history where we can see from the experience of Russia, Brazil, Argentina and even Greece that markets forgive and forget and base their investing decisions on the basis of what is to follow in the future, just as their current pricing of PIIGS debt and reluctance to lend is on the basis of future default, so will the markets AFTER default price and lend on the basis of future growth. The Bottom line is when Greece defaults, ALL of the other PIIGS will also quickly default, then it depends on what happens to other countries in and outside of the euro-zone on whether the systemic risk has been contained at that point, then you will see economic booms starting first in the defaulted PIIGS from their knocked down economic levels and soon spreading to countries that have stealth defaulted by means of Inflation such as the UK.

Protect Your Deposits From Bankrupting Banks

Your first priority must be to protect your deposits from Banks that could go bankrupt during a sovereign default induced global bank run, I last covered this in depth in June 2011 (Bankrupt Greece Blackmails Europe, Bailout or Euro Zone Dies, Global Financial System Collapse ), if you have not already done so then you need to act TODAY because amidst a banking crisis you may not get the opportunity to act.

My last article covered the risks per individual banks, however the truth is that in the event of a banking sector collapse - ALL DEPOSITS OVER THE £85k (100,000 Euro's) WOULD BE AT RISK as per government guarantee limits, so I am not going to repeat the analysis of stating the risks of individual banks, because the only truly SAFE UK bank is the 100% government backed National Savings and Investments.

Therefore KNOW THIS - IF the Banks in Europe Start to Collapse as a series of domino bank runs- NO DEPOSITS OVER £85k will be safe in ANY BANK other than National Savings & Investments.

Steps You Need to Take Now !

The following are my updated lists of tasks you need to do to protect your deposits because you are NOT being paid to carry the REAL RISK OF LOSS OF FUNDS ON DEPOSIT!

1. Ensure that you have at least 2 current accounts across banking groups and at least one with a safer bank such as HSBC.

2. Next make a list of all of your deposit / bank accounts, with the amounts on deposit.

3. Now group your accounts by banking sector group (see list here as a guide).

4. If you are anywhere near the £85k limit with any banking group then move those excess funds immediately!

5. Small banks and building societies are at greater risk than larger banks and building societies because the government is the larger banks such as HBOS pose a greater risk to the financial system and economy so the government will be more reluctant to let them fail, but that does not mean they will actually cover deposits beyond £85k in the event of a collapse, so you still need to limit exposure to £85k

6. Consider transferring funds to your spouse so as utilise their compensation limit across a banking group.

7. Ensure you have procedures in place so that you can at short notice transfer funds from high risk banks to lower risk banks so as to limit the fallout from any banking system crisis. For instance open an NS&I Direct Saver account NOW (pays 1.75% gross), then use this during an unfolding sovereign debt crisis event to transfer your cash to as this is the safest deposit account available for UK depositors (Max £2mill, Min £1). Again do this now as you may not be able to do so during a debt crisis event due to high demand for the account.

Instant Access Savings Accounts with Lower Risk banks

- NS&I - 1.75%

- Tesco - 2.90% (includes 1.65% bonus for 12 months)

- HSBC - 0.75% (includes 0.5% bonus if you do not withdraw in a calendar month)

Higher Risk banks

- Santander - 3.1% (includes 2.6% bonus for 12 months)

- Barclays - 1.25% (includes 0.35% bonus when you do not withdraw in a month).

- ING Direct - 3% (includes a 2.46% bonus if you do not withdraw in a month)

- SMILE (Co-op) 0.25%

Extreme High Risk Banks

- Halifax Online Saver - 2.8% (includes 2.7% bonus for 12months).

All accounts pay significantly less than current CPI Inflation of 5.2%.

8. Do not have ANY savings are fixed deposit exposure to banks that do not fall under the UK Financials Services Compensation Scheme.

9. Limit exposure to PIIGS banks, that is Greece, Ireland, Spain, Portugal and Italy as these are at the most risk of going bust thus triggering a lengthy process for savers having to wait for compensation. Remember that if Spain comes under pressure following perhaps Ireland and Portugal joining Greece, then the risks posed to Santander depositors will also significantly rise.

10. Keep enough in cash to cover at least 1 months expenditure, (I keep 2 months worth of cash).

11. Utilise instant transfer accounts between spouses, i.e. if you have accounts with the Halifax then you can instantly transfer funds between one another, therefore during a crisis you can instantly reduce the exposure if one person is above the £85k compensation limit at that time.

The bottom line, is if you want ZERO risk then dump all of your excess funds into National Savings & Investment accounts, for which the cost is 1.25% in terms of interest rate differentials.

Red Pill or Blue Pill ?

Do you want to continue sleep walking towards the total loss of the value of your wealth or walkup to the stealth inflation theft matrix?

This is what the worlds central bankers fear the most, that their respective populations wake up to the truth of the inflation mega-trend that they have been lied to for decades as to the real level of inflation that has forced them to work harder and borrow huge amounts to just maintain their standards of living.

They fear that workers will see through economic propaganda and start seeing the reality of what INFLATION is doing to them. THAT is the ONLY thing the likes of the Bank of England fears (well apart from banking sector induced financial armageddon) the workers of Britain starting to demand PAY rises that MATCH INFLATION AND TAX RISES (the wage price spiral).

Debt Deflation a Flawed Theory That Services the Purpose for Economic Propaganda

UK CPI Inflation smashed through the 5% barrier by rising to 5.2% for September (4.5%), which is now approaching near triple the Bank of England's 2% target that continues to make a mockery of the central bank whose primary remit is supposedly price stability, where 3% was supposed to have been the maximum level a break above which was supposedly to trigger a series of panic measures to bring inflation under control, instead of which the Bank of England has instead opted to print money as it recently announced another £75 billion of electronic money printing that the fractional reserve banking system would eventually leverage to over £1 trillion, for the primary objective for the monetization of government debt, i.e. the same policy that the Weimar republic had been engaged in on its path towards hyperinflation. UK public debt is probably being monetized at the rate of 15% per annum with approx 30% monetized to date, only the deflation fools and the vested interest academic economists cannot or choose not to realise the highly inflationary consequences of governments monetizing their debt.

Meanwhile the more recognised RPI Inflation measure surged higher to a 20 year high of 5.6% which is set against average pay rises of just 2% that illustrates an Inflationary Depression in progress.

CPI rising to above 5% should not come as any surprise as it has been expected to take place for several months now (14 Jun 2011 - UK CPI Inflation Holds at 4.5% as Stealth Theft of Wealth and Debt Default Continues )

UK CPI inflation looks destined to hit 5% within a few short months especially as energy companies continue to milk customers with outrageous unjustifiable price hikes of as much as 20%, all conducted in an environment of record low interest rates, now held at 0.5% for more than 2 years, all as a consequence of the Bank of England's primary focus in ensuring that the still bankrupt banking sector continues to generate artificial profits that are only partially being used to write down bad debts, with the balance paid out as bonuses on what amount to fictitious tax payer funded profits.

UK inflation has soared to above my already high expectations as per the January forecast for 2011 (17 Jan 2011 - UK Inflation Forecast 2011, Imminent Spike to Above CPI 4%, RPI 6% ) that expected Inflation to remain above Bank of England's 3% upper limit for the whole of 2011, which is set against the Bank of England's Feb 2011 Inflation Report that expected CPI of just 1.7% by the end of 2011.

However, actual inflation as experienced by most people in Britain currently stands at an even hideously higher rate of 7.36%, which explains why your weekly groceries bill is inflating at a rate twice the official inflation indices that have been manipulated by successive governments to under-report the true rate of inflation. According to the debt deflation theory we should have had deflation for the past 2 years, instead of high inflation in consumer prices. The reason why is obvious in that the economic models are FLAWED, the reality is this, which not something new but something I have repeatedly iterated for 2 years now and that is that ALL FIAT CURENCIES ARE IN FREEFALL AGAINST ONE ANOTHER ! Which means exchange rates may give the illusion of currency stability but the reality of the overall trend is that ALL currencies are FALLING at an exponential rate ! Which is why you have compound inflation i.e. the trend for the inflation curves are exponential. This is why as savers and investors you need to leverage yourself to the Inflation mega-trend because deflation will not be allowed to exist in our fiat currency fractional reserve banking money printing world, regardless of what the debt deflation theory of ivory tower academics state should take place. The bottom line is that some 2 years on from my initial warning (18 Nov 2009 - Deflationists Are WRONG, Prepare for the INFLATION Mega-Trend ), debt deflation remains and has shown it self to be a red herring! The real world example of Iceland illustrates the consequences of the collapse of currency where despite soaring unemployment and a contracting economy they had inflation soaring to 20%! DEPRESSION - YES DEFLATION - NO What you get is an INFLATIONARY DEPRESSION, which the UK clearly exemplifies with rising unemployment, and a stagnating economy and ACCELERATING ANNUALLY COMPOUNDING INFLATION. DEPRESSION DESTROYS DEMAND, RESULTING IN UNEMPLOYMENT That does not mean supply will result in falling prices, because DEPRESSION DESTROYS SUPPLY, RESULTING IN UNEMPLOYMENT Unemployment results in higher government spending / deficits resulting in more money / debt printing resulting accelerating drop in the fiat currency (does not matter what it does relative to others, as all currencies are in perpetual free fall against one another). Therefore a falling currency results in RISING PRICES REGARDLESS OF ECONOMIC THEORY, REGARDLESS OF THE DESTRUCTION OF DEMAND, REGARDLESS OF THE RISE IN UNEMPLOYMENT AND REGARDLESS OF THE DESTRUCTION OF CREDIT! Global Occupy Wall Street Comes to London The injustice of the workers, students, retirees and savers being forced to pay for the crimes of politicians and bankster's has come to London with demonstrations across the financial district of London.

The demonstrators seek greater equality in the distribution of wealth as they see the top 1% get richer whilst the rest suffer during the economic depression which is where Britain and most of the western world have drifted into.

However, the demonstrators appear confused as to who is actually to blame because most of their slogans put the blame at the foot of capitalism, when capitalism is not to blame but politicians and the bankster elites as a consequence of the fractional reserve banking system that is designed to turn everyone and everything into debt slaves that requires the inflation stealth tax to function as I covered at length recently (Bank of England's Quantitative Inflation Bankster's Paradise Inflationary Depression Economy ).

At worst the multi-nationals are to blame for off shoring jobs, but all corporations are charged with maximising profit for their share holders.

The real problem is that people in the west are being over paid, this is part of the mega-trend for the convergence of GDP between the developed and developing world which no government can fight against, basically because there are workers in countries such as China, India, and Brazil who are doing the same jobs as those in the in west for 1/10th of the pay.

This is not just west vs east mega-trend but we see it in Europe today where the likes of Greek public sector workers protesting against downward pressure on wages whilst they are being paid as much as six times as public sector workers doing the same jobs in other european countries such as the Czech republic.

So in many respects the Occupy Wall Street have it wrong, they are fighting to maintain jobs especially in the public sectors that the countries cannot afford and only finance through debt. In fact many of the demonstrators need to fight for less debt and borrowing rather than more for there is no free lunch, all borrowing more money will do is to increase the real rate of inflation, thus making the workers and savers poorer. Protect Your Wealth From the Quantitative Inflation Mega-trend

The crisis is that the bankrupt banks have bankrupted virtually every western nation. The advantage for the likes of the UK and USA is that these countries are stealthily defaulting on their debts and liabilities by printing money and inflating the debt away as real inflation stands several points above the official indices, something that each and everyone experiences when we go to shop for goods and services. Whilst this avoids the loss of the value of your savings in nominal terms however over the course of INFLATION MEGA-TREND 2010's decade, the value of your savings will STILL BE WIPED OUT because at the end of the day the price is and will continue to be paid by savers and workers in loss of purchasing power of accumulated wealth and earnings.

Contrary to government and central bank propaganda, high inflation is here to stay because : a. It is a government stealth tax on the workers and savers that especially hits the middle classes hard as it is a mechanism for the transference of wealth to all those who are in receipt of government handouts be they the bankster elite or those on benefits. b. It is for the purpose for the stealth default on total UK debt (Public+private+unfunded liabilities), that totals in the region of £11 trillion. As a reminder that despite all of the economic propaganda the Coalition government has so far NOT PAID DOWN ANY DEBT, instead debt continues to accumulate at the approx rate of £140 billion a year. The reason for this is simple because the government is not experiencing any financing pain for new borrowings, i.e. 10 year gilt yields are trading at 2.5%, looking at this from another angle, this means investors are willing to loan the UK government money for 10 years at 2.5%, in which case the UK government as would be the case with any borrower, is effectively in receipt of free money as inflation is running at twice the rate of interest charged. Off course this is not sustainable as countries such as the PIIGS have found out, there is always a crunch point when the market wakes up and is no longer willing to finance un payable borrowings. Therefore a 5.6% RPI means that the value of total UK debt is being devalued and stealthily defaulted on at the rate of £616 billion which is MORE than TOTAL Government Revenues of some £500 billion.

Which is why regardless of what you will read in the mainstream press INFLATION IS the PRIMARY FORM OF TAXATION IN THE UK, that exceeds ALL other taxes put together.

That is why Inflation is perpetual, forever, given the huge benefit enjoyed by government and why all the talk of inflation falling is just worthless propaganda because the government wants / needs inflation. This is something that I espoused right at the very beginning of the current phase of the perpetual inflation mega-trend in January 2010 Inflation Mega-trend ebook (FREE DOWNLOAD).

Therefore the coalition government, as is the case with every government is ONLY focused on one thing and that is to get re-elected, and to achieve this it has to borrow and spend enough money to generate the illusion of economic prosperity in the last year or 2 into the lead up to the next election. My next series of articles will seek to update the Inflation Mega-trend wealth protection strategies such as Housing (people waiting for prices to fall are forgetting about the effect of inflation), Stocks (summer correction clearly looks over, dividend increasing stocks are leveraged to the inflation mega-trend ) and Commodities (whilst you can mine gold and silver they can't be printed, though oil and agriculture are probably better long-term bets because they are consumed). So ensure you are subscribed to my always free newsletter to get these in your email in box.

Your wealth protecting inflation mega-trend analyst.

By Nadeem Walayat

Copyright 2012 WalayatFamily.com - All Rights Reserved